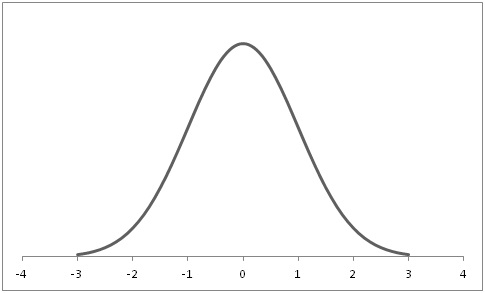

Key properties of the normal distribution

CFA level I

/

Quantitative Methods: Application

/

Common Probability Distributions

/

Key properties of the normal distribution